Foreign Tax Credits Explained: How to Limit Exposure to Double Taxation on Cross-Border Income

March 12, 2026

Article Overview:

The Foreign Tax Credit (FTC) is the primary tool for mitigating double taxation on global income. However, with new "basketing" rules and the 2026 overhaul of GILTI into NCTI, navigating the IRC § 901 regime requires more than just a math calculation; it requires a proactive legal strategy.

I. The Double Taxation Dilemma: Why the FTC Is Your Global Shield

For any U.S. person earning income abroad, whether through a foreign rental property, a cross-border business, or international investments, the threat of double taxation is a constant reality.

The United States imposes tax based on citizenship and residency, meaning U.S. citizens and resident aliens are generally taxed on their worldwide income, regardless of where they live or where the income is earned. U.S. entities, such as domestic corporations and partnerships, are also generally subject to U.S. taxation on their worldwide income. At the same time, the country where the income is generated, the source country will typically impose its own tax.

Without relief, these competing claims could produce a combined tax burden exceeding 50% or more, significantly reducing the profitability of international activities.

The Foreign Tax Credit (FTC), governed primarily by IRC § 901, is designed to mitigate this problem. The FTC generally provides a dollar-for-dollar credit against U.S. tax liability for qualifying income taxes paid to a foreign government.

However, the FTC is not automatic. Complex rules, particularly those governing foreign-source income, separate limitation categories (“baskets”), and the IRC § 904 limitation formula, can restrict the amount of credit available, turning a straightforward benefit into a complex international tax planning exercise.

For taxpayers with international income, understanding these rules is essential to preventing unnecessary double taxation.

II. When Is a Foreign Tax “Creditable”?

Not every payment to a foreign government qualifies for a foreign tax credit. In general, a foreign tax must satisfy several requirements:

1. The Tax Must Be an Income Tax (or a Tax in Lieu of an Income Tax)

The foreign levy must be based on net income or profits in a manner similar to a U.S. income tax. Taxes such as VAT, sales taxes, customs duties, and wealth taxes generally do not qualify.

2. The Tax Must Be Compulsory

The tax must be a legal and actual liability under foreign law. Voluntary payments or amounts eligible for refund generally cannot be credited.

3. The Tax Must Be Paid or Accrued

Taxpayers may claim the FTC on either a paid basis or an accrual basis, depending on their election.

4. The Tax Must Be Imposed on the Taxpayer Claiming the Credit

Although the tax may be withheld at source (for example, by a bank or employer), the taxpayer must be the party legally responsible for the tax.

Alternative: Deduction Instead of a Credit

If a foreign tax does not qualify for a credit, it may still be deductible as an itemized deduction. However, a deduction reduces taxable income rather than tax liability, making it generally less valuable than a credit.

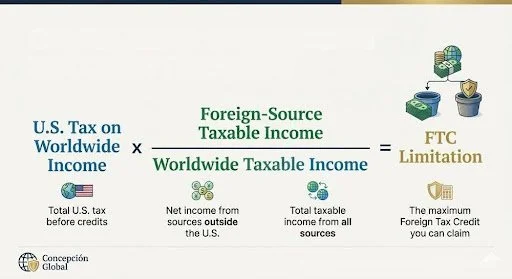

III. The FTC Limitation: Why You May Still Owe the IRS

Even if you paid substantial tax abroad, the United States does not allow unlimited foreign tax credits.

Under IRC § 904, the FTC is limited to the amount of U.S. tax attributable to foreign-source income.

The basic limitation formula is:

FTC Limitation = U.S. tax liability × (Foreign-source taxable income ÷ Worldwide taxable income)

This limitation is calculated separately for each income basket and reported on IRS Form 1116, which most individual taxpayers must file to claim the credit. If the foreign tax rate exceeds the U.S. rate, taxpayers may accumulate excess foreign tax credits. If the foreign rate is lower, the taxpayer may owe residual U.S. tax on the income.

IV. Income “Baskets”: Why Categorization Matters

FTC calculations must be performed separately for different categories of income, commonly referred to as “baskets.”

This prevents taxpayers from using high foreign taxes on one type of income to offset U.S. tax on another.

The primary categories include:

Passive Category Income

Typically includes dividends, interest, royalties, and certain rents.

General Category Income

Generally includes wages, salary, and active business income not falling into another category.

Foreign Branch Category Income

Income attributable to a foreign branch or qualified business unit (QBU) operating outside the United States.

Because the FTC limitation applies separately to each basket, careful classification of income is essential to maximizing credits.

V. Special Rules for Owners of Foreign Corporations

Taxpayers who own controlled foreign corporations (CFCs) may encounter additional FTC rules related to tested income under IRC § 951A.

For tax years beginning after December 31, 2025, legislative changes rename the GILTI regime as Net CFC Tested Income (NCTI). These rules involve specialized foreign tax credit mechanics that differ from the standard Form 1116 regime applicable to individuals with wages, rental income, or portfolio investments.

Because the interaction between CFC ownership, tested income, and foreign tax credits is complex, these situations often require individualized planning.

VI. FTC vs. the Foreign Earned Income Exclusion (FEIE)

For Americans living abroad, the most important annual tax decision is often whether to claim the Foreign Earned Income Exclusion (FEIE) or rely primarily on the FTC.

For 2026, the FEIE allows eligible taxpayers to exclude up to $132,900 of foreign earned income.

In general:

FEIE may be advantageous when:

The taxpayer resides in a low-tax jurisdiction

Most income is earned income (salary or self-employment)

FTC may be preferable when:

The taxpayer resides in a high-tax country

The taxpayer has significant passive income

Foreign taxes exceed U.S. rates

Importantly, the FEIE applies only to earned income, not passive income such as dividends or rental income.

If a taxpayer revokes the FEIE, they generally cannot claim it again for five tax years without IRS consent, making the choice particularly significant.

VII. Carrybacks and Carryforwards

If foreign taxes exceed the FTC limitation, the unused credits may still provide future benefit.

Under current law:

Excess credits may be carried back 1 year

Excess credits may be carried forward up to 10 years

However, taxpayers must track these carryovers carefully, typically using Form 1116 schedules. Failure to maintain proper documentation can result in losing the ability to claim the credit in future years.

VIII. The Role of Tax Treaties

U.S. [tax treaties] can also help mitigate double taxation. Many treaties include re-sourcing provisions, which allow certain income that would otherwise be treated as U.S.-source income to be treated as foreign-source income for FTC purposes.

This can be critical because foreign tax credits can only offset U.S. tax on foreign-source income.

Treaty interpretation, however, is highly fact-specific and depends on the relevant treaty article.

IX. Practical Planning Steps

Taxpayers with international income should consider several proactive strategies:

Review Withholding Rates

Ensure that the correct documentation—such as Form W-8BEN or treaty forms—is provided to claim reduced withholding rates where applicable.

Evaluate the Paid vs. Accrued Method

Electing to claim credits on an accrual basis can help align foreign taxes with the income they relate to, although it may create additional compliance obligations.

Analyze Entity Structures

Owners of foreign businesses should evaluate whether entity classification elections (“check-the-box”) may improve FTC utilization.

Maintain Documentation

The IRS often audits FTC claims. Taxpayers should retain foreign tax returns, withholding statements, and proof of payment.

Conclusion: Strategic Planning Is Essential

The Foreign Tax Credit is one of the most powerful tools available to mitigate international double taxation. However, it is far from automatic.

The interaction of sourcing rules, limitation formulas, income baskets, and treaty provisions means that errors in classification or documentation can permanently reduce available credits.

For individuals and businesses with cross-border income, proactive planning and careful compliance are essential to ensuring that global income is taxed fairly—and not twice.

If you are managing significant global assets, it is time to seek specialized tax counsel to optimize your structure and protect your hard-earned returns from the erosion of double taxation.

For customized tax advice, contact Christine Alexis Concepción at caconcepcion@concepcionlaw.com.